The Know Your EdTech database tracks 79 edtech companies and over 200 products for young children (0-8) in Australia. The market splits into domestic edtech (aimed at families with parents as buyers) and institutional edtech (used by early childhood professionals and educators). Here are some findings from our study conveyed in visuals.

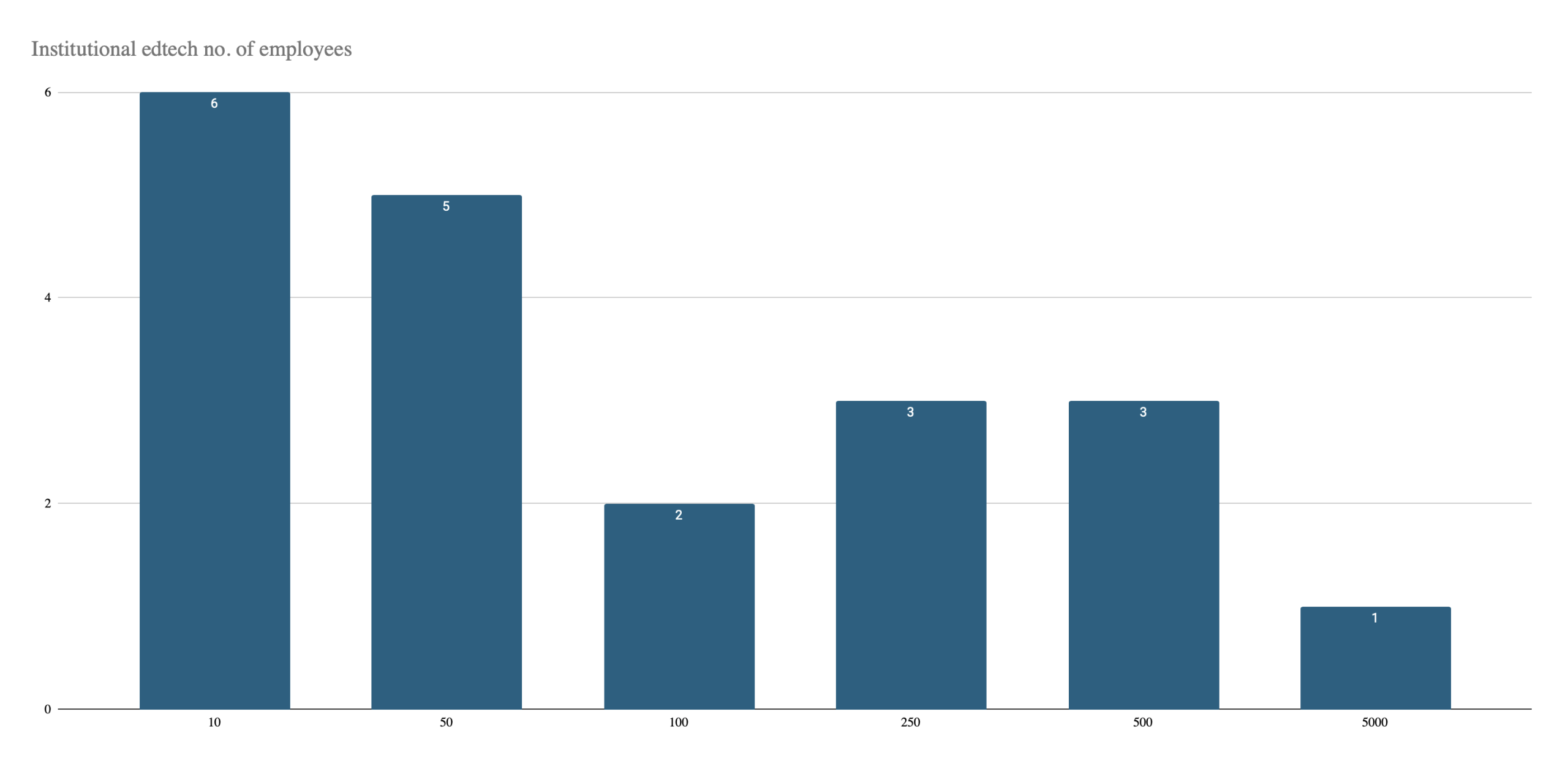

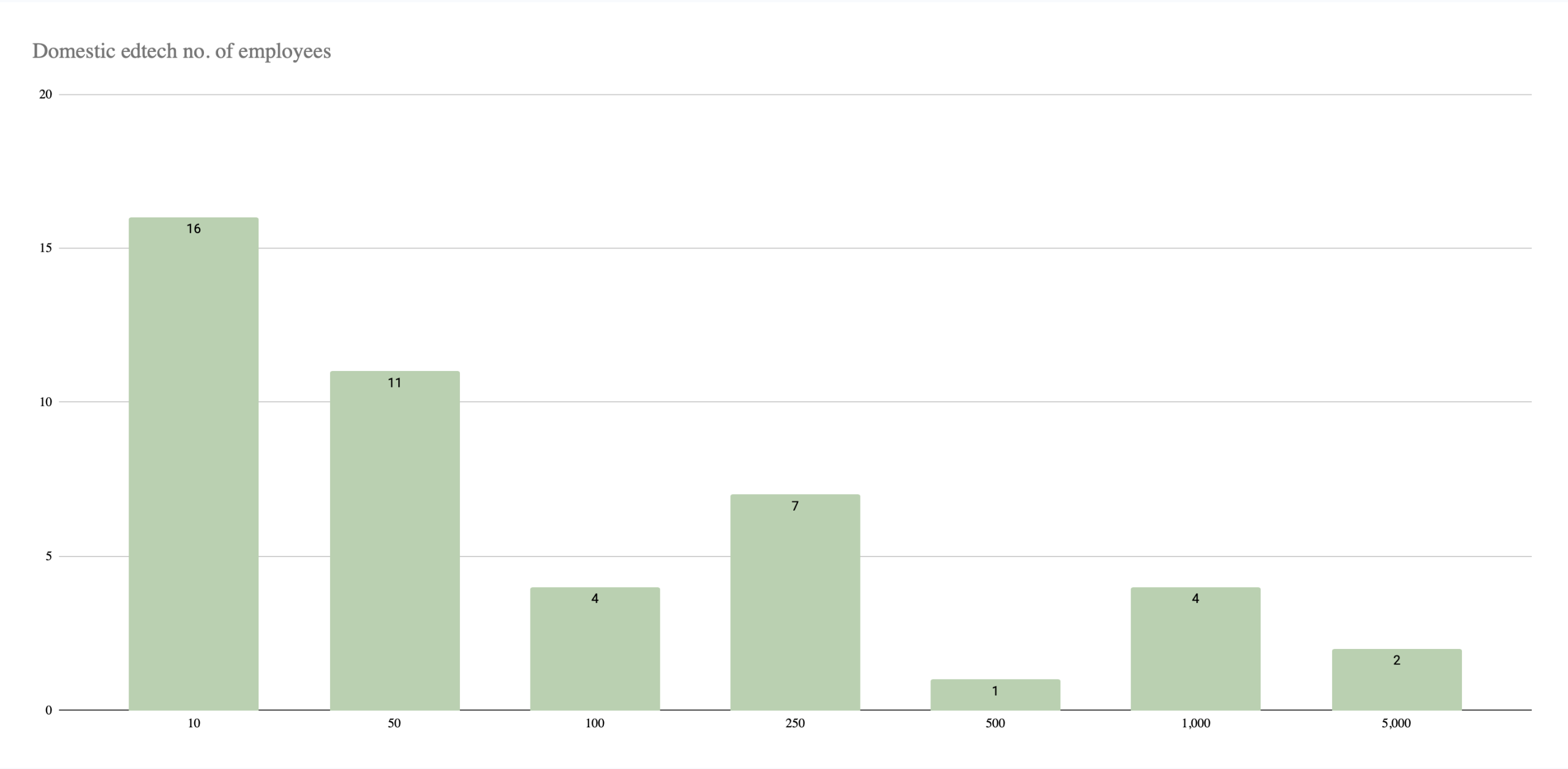

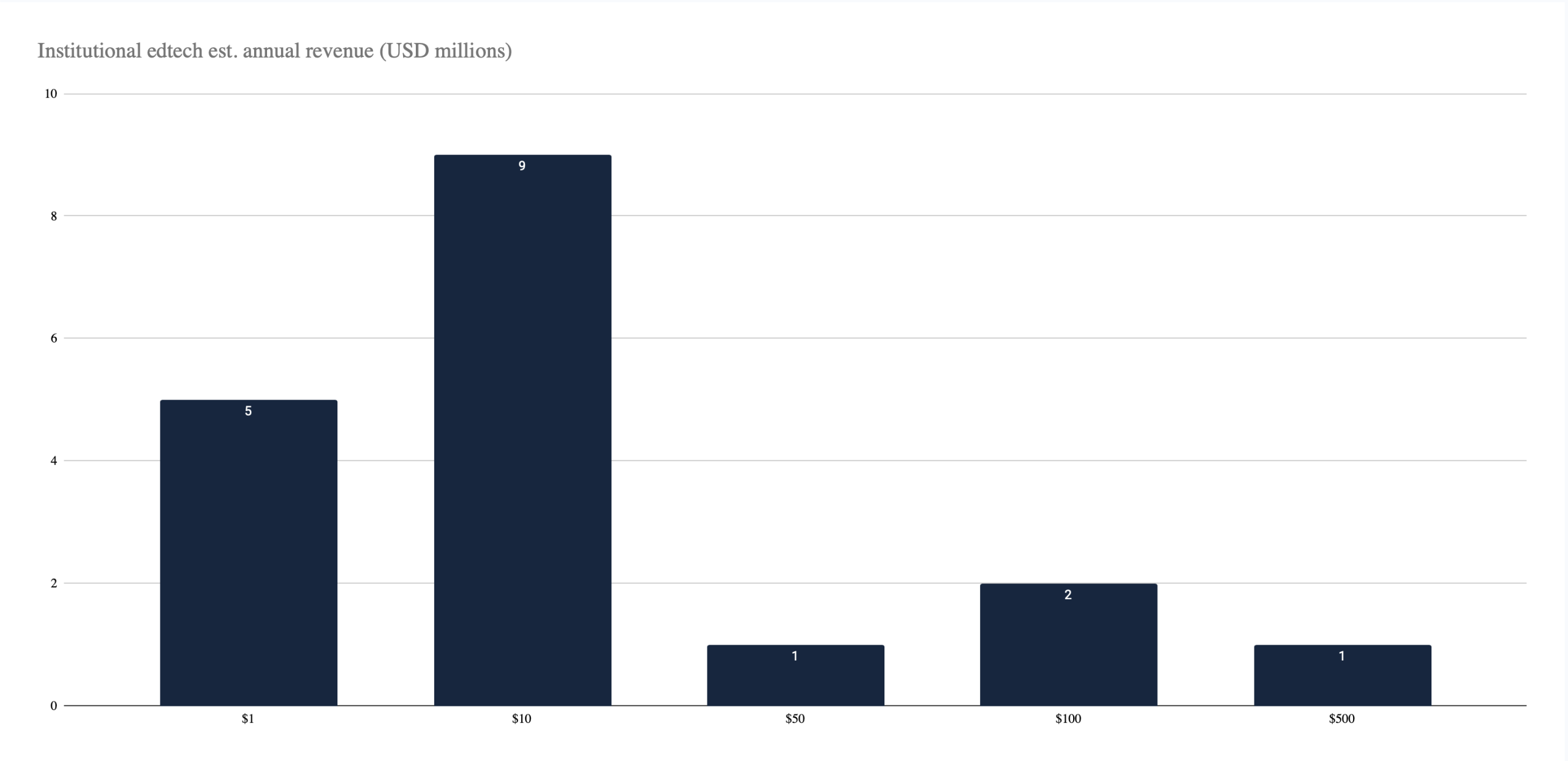

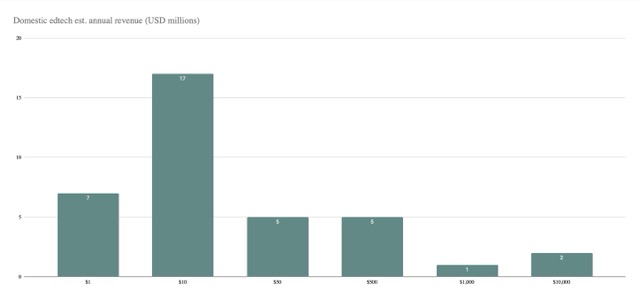

1. How big are edtech companies?

We looked at both the size and revenue of institutional and domestic edtech companies. We discovered that almost half of the companies in our database have fewer than 50 employees—a notable insight given the dominance of large tech corporations in the broader edtech sector (Williamson 2022). In terms of revenue, most companies are making below $10 million USD annually. In addition, based on annual revenue, there is some early indication that the market for domestic edtech products is more profitable to the institutional edtech market.

2. Where are edtech companies located?

Here is an interactive map showing the locations of edtech companies through orange (institutional) and blue (domestic) dots. The map also visualises the countries of origin and summarises the number of companies. What city is your favourite app being developed in?

The institutional edtech market is primarily local or regional, likely influenced by regulatory requirements (Pangrazio and Bunn 2024) and the prevailing belief that formal education should be tailored and governed by national curricula. In contrast, the domestic edtech market—often characterised by gaming components—is increasingly global, as parents present accessible audiences for global tech companies.

Does is matter where the company behind an app or product is located?

3. What ‘educational’ app are popular?

Although the domestic edtech market is dominated by US-based companies, the most popular apps do not come from American companies. Notable examples include China’s Babybus and South Korea’s The Pinkfong Company, which have developed some of the leading apps. Additionally, Norway’s Kahoot! has recently entered domestic edtech markets, while Spanish developer Monkimum Labs, creators of Lingokids, continues to expand its presence.

| Downloads | Company | Country | ||

|---|---|---|---|---|

|

Baby Panda World | 100M | Babybus | |

|

Toca Boca Jr | 100M | Piknik | |

|

Toca Boca World | 100M | Toca Boca | |

|

Pinkfong Baby Shark | 50M | The PinkFong Company | |  |

LingoKids | 50M | Monkimum Labs |

|

Toca Boca Hair Salon 4 | 50M | Piknik | |

|

Miga Town My World | 50M | Xihe Digital | |

|

Bebi: Baby Games for Toddlers | 10M | Bebi Family Games | |

|

Toddler educational games 2-4y | 10M | Bebi Family Games | |

|

Learning games for toddlers 2+ | 10M | Bimi Boo |

Based on data from Google Play (updated in May 2026)

Do you find the these most downloaded apps educational? Are you more likely to download apps with a high number of downloads?

4. Who invests in edtech?

This interactive diagram shows the organisations that have invested funds or other resources into domestic edtech. In this figure, edtech companies and their investors are connected through grey lines; in most cases, one edtech company is connected with multiple investors. If you click on an investor or a company, you can see the connections yourself. For instance, Global 500 (a venture capital firm) has invested in the companies behind Epic! but also in LingoKids.

Investment funds or firms that provide capital to early-stage, high-growth companies in exchange for equity, typically seeking high returns through eventual company growth or exit. Research has pointed out that while VC investors are relatively new financial actors in education, they are distinctive in that ‘they provide finance in search of return on investment (ROI) and impact on the actions of their investees’ (Komljenovic et al., 2023, p. 2).

An investor or investment firm that focuses exclusively on funding companies in the education technology sector.

Organisations that reinvest any surplus revenues to further their educational or social mission rather than distributing profits to shareholders or owners.

Programmes or organisations that provide early-stage companies with mentorship, resources, and seed funding, often in exchange for equity, to accelerate their growth over a fixed period.

Individuals who invest their personal funds into startups, usually in the early stages, in exchange for equity or convertible debt, and often provide mentorship as well.

A business owned by private individuals or groups that does not publicly trade shares on the stock market; may invest in or operate edtech ventures.

Public sector bodies or agencies that support edtech through funding, policy initiatives, or direct investment, aiming to foster innovation or meet educational goals.

Higher education institutions that may invest in, incubate, or partner with edtech startups to promote research, innovation, or improved educational outcomes.

Both submarkets are mainly driven by venture capital investors (n=84), indicating the edtech market is still emerging and unstable. As with Finding #1, domestic edtech attracts more interest than institutional edtech, likely due to varying consumer purchasing power investors. There is a small proportion of ‘edtech-specific investors'(8) which raises concerns about the educational expertise and experience of general investors compared to the edtech-specific investors.

It is worthing noting that there is still a small representation of not-for-profit organisations, government initiatives and university funding. For example, well-known groups like LEGO Foundation or Black Ambition are present in our sample. We can also see government support for companies like Shoelace Learning from the Atlantic Canada Opportunities Agency (ACOA) and the Canadian Government. Other firms like Lingokids derived support through the Horizon 2020 Research Grant from the European Commission receiving a $1.1 million grant in 2018 which they used to expand its proprietary ‘Playlearning’ methodology.However, in general, the role of not-for-profit and government funding bodies is negligible, compared to the quantity of for-profit investors.

Does it matter who the investors behind apps or edtech products are?